41 defined contribution pension death

Defined contribution pensions - BDO Defined contribution pensions - retirement and inheritance planning Relaxation of tax charges for pension funds on death after age 75. It has long been the case that if an individual dies... Planning considerations. This means that members of a defined contribution (DC) scheme can now nominate ... Death benefits from defined contribution schemes Death benefits from occupational defined contribution schemes may not offer full flexibility of death benefits. Death benefits are usually tax-free if the member dies when they are under 75, they are settled within two years of the scheme administrator becoming aware and the lump sum is within the member's lifetime allowance.

Triviality and commuting small pensions for cash Small pensions from both defined benefit and/or defined contribution schemes, payable to a survivor on the death of member can be commuted and paid as a one off lump sum (known as a trivial commutation lump sum death benefit) provided the value of the lump sum in each scheme is no more than £30,000.

Defined contribution pension death

Retirement Topics - Death | Internal Revenue Service Retirement Topics - Death. When a participant in a retirement plan dies, benefits the participant would have been entitled to are usually paid to the participant's designated beneficiary in a form provided by the terms of the plan (lump-sum distribution or an annuity). ERISA protects surviving spouses of deceased participants who had earned a vested pension benefit before their death. PDF Defined Benefit Plan Beneficiary Nomination Form Your designations on this form apply only to your SERS defined benefit pension. You must file a separate form to designate beneficiaries for any other retirement benefits, including SERS-administered defined contribution and deferred compensation plans. Because SERS will pay your death benefit according to your stated intent, it is Defined Contribution Pension Plan (DC) | Human Resources ... The Defined Contribution (DC) Component of the University of Winnipeg Trusteed Pension Plan was established effective January 1, 2000. The purpose of the Defined Contribution Pension Plan is to help you save for retirement. The Plan provides investment options, tax sheltering of assets and investment earnings until retirement.

Defined contribution pension death. Types of private pensions - GOV.UK Defined contribution pension schemes These are usually either personal or stakeholder pensions . They’re sometimes called ‘money purchase’ pension schemes. What happens to my pensions after death? | The Private Office If you have built up substantial funds in your pensions during your working life and have not taken any benefits from them and subsequently die before your 75th birthday your defined contribution pension funds and any defined benefit lump sums will be tested against your Lifetime Allowance. Defined-Contribution Plan Definition The defined-contribution plan differs from a defined-benefit plan, also called a pension plan, which guarantees participants receive a certain benefit at a specific future date. Death Benefits - Defined Contribution Schemes Death Benefits - Defined Contribution Schemes A look at how pension benefits can be distributed on death and their tax treatment. A look at how pension benefits can be distributed on death and their tax treatment. Key Points Individuals can nominate anyone to receive their pension death benefits.

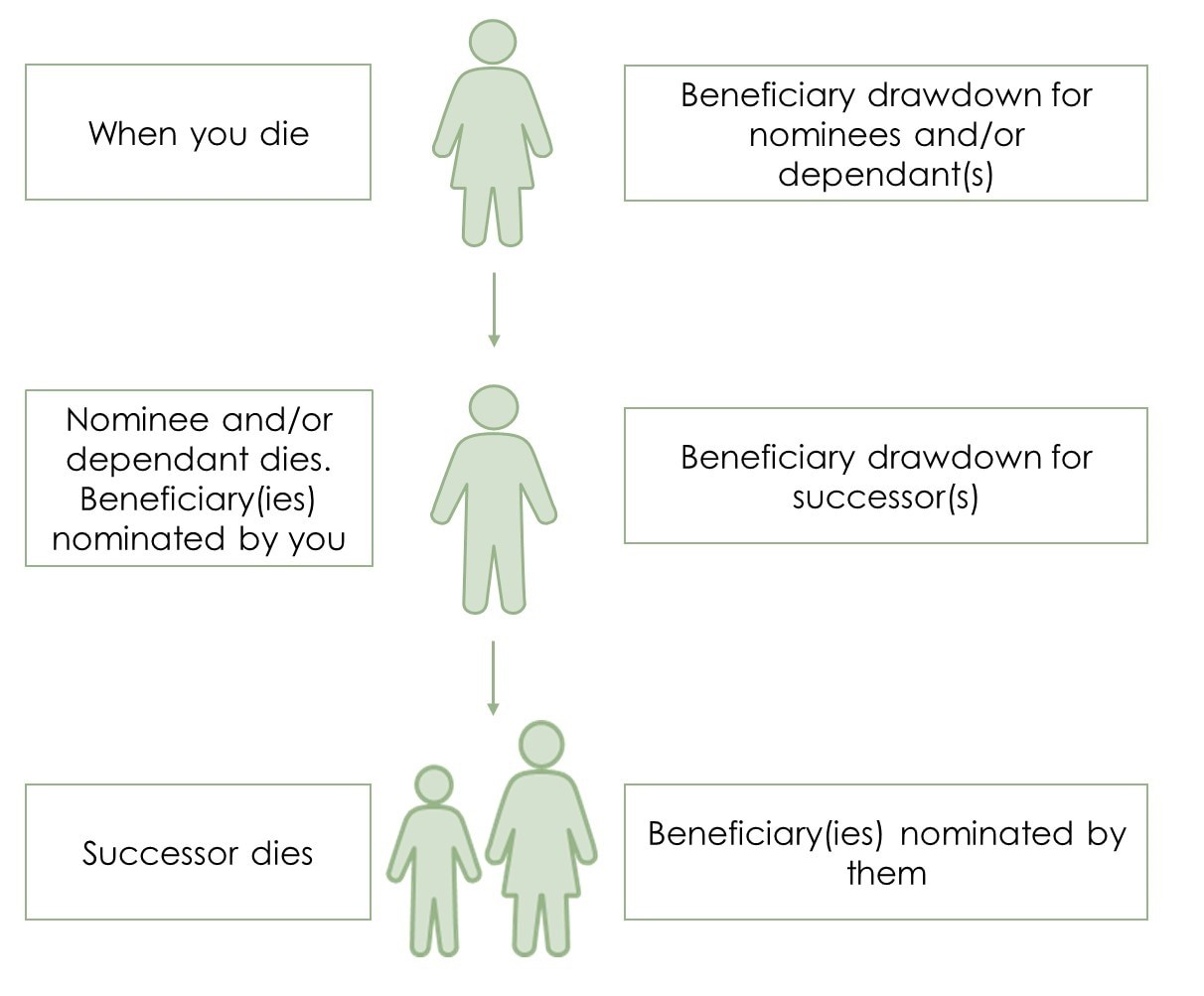

Death benefits from a defined benefit pension scheme | Tax ... Death benefits from a defined benefit pension scheme Introduction. On the death of a scheme member or a beneficiary, a registered pension scheme is only authorised to pay out benefits to a beneficiary either as a pension death benefit or as a lump sum death benefit. Inherited Pension Benefit Payments From Deceased Parents Apr 25, 2021 · Defined-Contribution Pension . With a defined-contribution plan, such as a 401(k), the beneficiary can access remaining funds in the retirement account via a gradual drawdown, lump sum payment, or ... PDF Defined Contribution Pension Plan Death Benefit Application Defined Contribution Pension Plan Death Benefit Application _____ Complete all applicable sections and return pages 1-3 to: Southern California Pipe Trades Administrative Corporation Defined Contribution Department 501 Shatto Place, 5th Floor Los Angeles, CA 90020 Save "Your Rollover Options" for your records. (800) 595-7473 OR (213) 385-6161 Death benefits for defined benefit schemes Defined benefit schemes usually offer lump sum death benefits and scheme pension. The lump sum death benefit will usually be a set amount or a multiple of salary. Lump sum death benefits are tax-free if the member dies under age 75, the lump sum is within the member's lifetime allowance and it is paid within two years of the scheme administrator becoming aware of death.

DEFINED CONTRIBUTION PENSION - A Complete Guide As with a defined contribution pension, your contributions are tax-free. But like a defined benefit pension, you are guaranteed a certain amount by the pension provider when you ultimately retire. The pension provider has a team of investment managers to earn a return. They put your money to work by investing in shares and other assets. Tax on a private pension you inherit - GOV.UK Passing on a pension pot you inherited If you inherit a defined contribution pot you can nominate someone to get any money you do not use before your death. The money must be in a flexi-access... What happens to my pension when I die? | MoneyHelper Defined benefit pension schemes might also pay a refund of the contributions paid by the member, if the member dies before starting to draw their pension. This is subject to the scheme's rules. Interest might also be added to the refund of contributions under some scheme's rules. Pension protection lump sum Defined contribution pension options at retirement ... When you retire from a Defined Contribution Pension Plan, your retirement options are very different than the options from a Defined Benefit Pension Plan. The pension options you have will depend on a few different things but the biggest issues are the amount of money you have in the pension and your age.

I'm not in a Clarks pension scheme - Clarks

What happens to your pension when you die? - Aviva A defined contribution pension — a pension that's based on how much has been paid into it — will normally pay the value of your pension pot in a lump sum to your dependants. If you die before age 75, benefits under money purchase schemes can usually be passed on to your beneficiaries free of tax.

The Death of the Pension Fund - Next Generation Trust Company

Pensions and inheritance - Unbiased.co.uk This assumes you have a defined contribution (money purchase) pension scheme, which is the case for most workplace pensions and all private pensions. Note that this only holds true if you have unspent pension pot remaining.

General Dynamics United Kingdom Retirement and Death Benefit ...

What is a defined contribution pension? | PensionBee A defined contribution pension is the most common type of pension. On retirement, the amount your defined contribution pension is worth depends on how much money you've contributed and the performance of your investments. Most modern workplace and personal pensions are defined contribution pensions. Building up your defined contribution pension

My partner or someone in my family has died - what do I do ...

Defined contribution schemes - The Pensions Authority Defined contribution (DC) schemes are occupational pension schemes where your own contributions and your employer's contributions are both invested and the proceeds used to buy a pension and/or other benefits at retirement. The value of the ultimate benefits payable from the DC scheme depends on the amount of contributions paid, the investment return achieved less any fees and charges, and the cost of buying the benefits.

Extension of benefits of "Retirement Gratuity and Death ...

Defined Contribution Pension Plan in Canada: Complete Guide Example of a Defined Contribution Pension Plan. Let's consider Michael. Michael is an employee for a renowned business earning a good salary at the company. The organization employs the Defined Contribution Pension Plan for its employees, and Michael opts for it. According to the plan, he makes a contribution of $2,000 in a year.

INFORMATION NOTE ON THE NATO DEFINED CONTRIBUTION PENSION ...

What happens to your pension when you die? | PensionBee Defined contribution pensions. The main pension rule governing defined contribution pensions in death is your age when you die and whether you've already started drawing your pension. If you die before your 75th birthday and haven't started drawing your pension it can be passed to your beneficiaries tax-free.

What is the impact of the pensions lifetime allowance on ...

Defined Contribution Plan In a defined contribution plan, the employer and employee contribute a set or defined amount and the amount of pension income that the member receives upon retirement is determined by, among other things, the amount of contributions accumulated and the investment income earned.These contributions are often a fixed percentage of an employee's annual earnings and are deposited monthly in an ...

First Actuarial on CDC (submission to W&P Select). | AgeWage ...

Defined Contribution Pension schemes What is a defined contribution pension ? Defined contribution pensions can be: workplace pension schemes set up by your employer, or private pension schemes set up by you. If you're a member of a pension scheme through your workplace, then your employer usually deducts your pension contributions from your salary before it is taxed.

Defined Benefits Pensions – What should you do? - ppt download

Pension Funds Novartis · Death Pension Funds Novartis · Death Death The death of a loved one is associated with grief and pain. At the same time, one is confronted with numerous formalities. The following information is intended to help you take the necessary steps with the Novartis Pension Funds. Notification of Novartis Pension Funds

Not Your Father's Pension Plan: The Rise of 401(k) and Other ...

Transfer of Pension Assets - Dynamic Defined Benefit Pension Plan. This is the type of plan where a formula outlines how much you will be paid at retirement. As with Defined Contribution plans, the benefit received by the widow/widower depends on if the death occurred before or after the pension payments begin. Death before pension payments begin. Two options may be available.

B.A.C. TRUST FUNDS

Pension death benefits 'indefensibly generous' | Financial ... Rule changes in 2015 allowed any unused cash left in a defined contribution personal pension to be passed to beneficiaries and heirs tax free if the pension holder died before the age of 75.

Death benefits: discretion or direction? - Royal London for ...

Defined Contribution Pension Plan (DC) | Human Resources ... The Defined Contribution (DC) Component of the University of Winnipeg Trusteed Pension Plan was established effective January 1, 2000. The purpose of the Defined Contribution Pension Plan is to help you save for retirement. The Plan provides investment options, tax sheltering of assets and investment earnings until retirement.

New planning horizons in a world of Pension Freedom? - ppt ...

PDF Defined Benefit Plan Beneficiary Nomination Form Your designations on this form apply only to your SERS defined benefit pension. You must file a separate form to designate beneficiaries for any other retirement benefits, including SERS-administered defined contribution and deferred compensation plans. Because SERS will pay your death benefit according to your stated intent, it is

Germany

Retirement Topics - Death | Internal Revenue Service Retirement Topics - Death. When a participant in a retirement plan dies, benefits the participant would have been entitled to are usually paid to the participant's designated beneficiary in a form provided by the terms of the plan (lump-sum distribution or an annuity). ERISA protects surviving spouses of deceased participants who had earned a vested pension benefit before their death.

Untitled

Solved DQuestion 21 1 pts Su-Hyon says, "I want a retirement ...

Letter to Active Members - The United Church of Canada

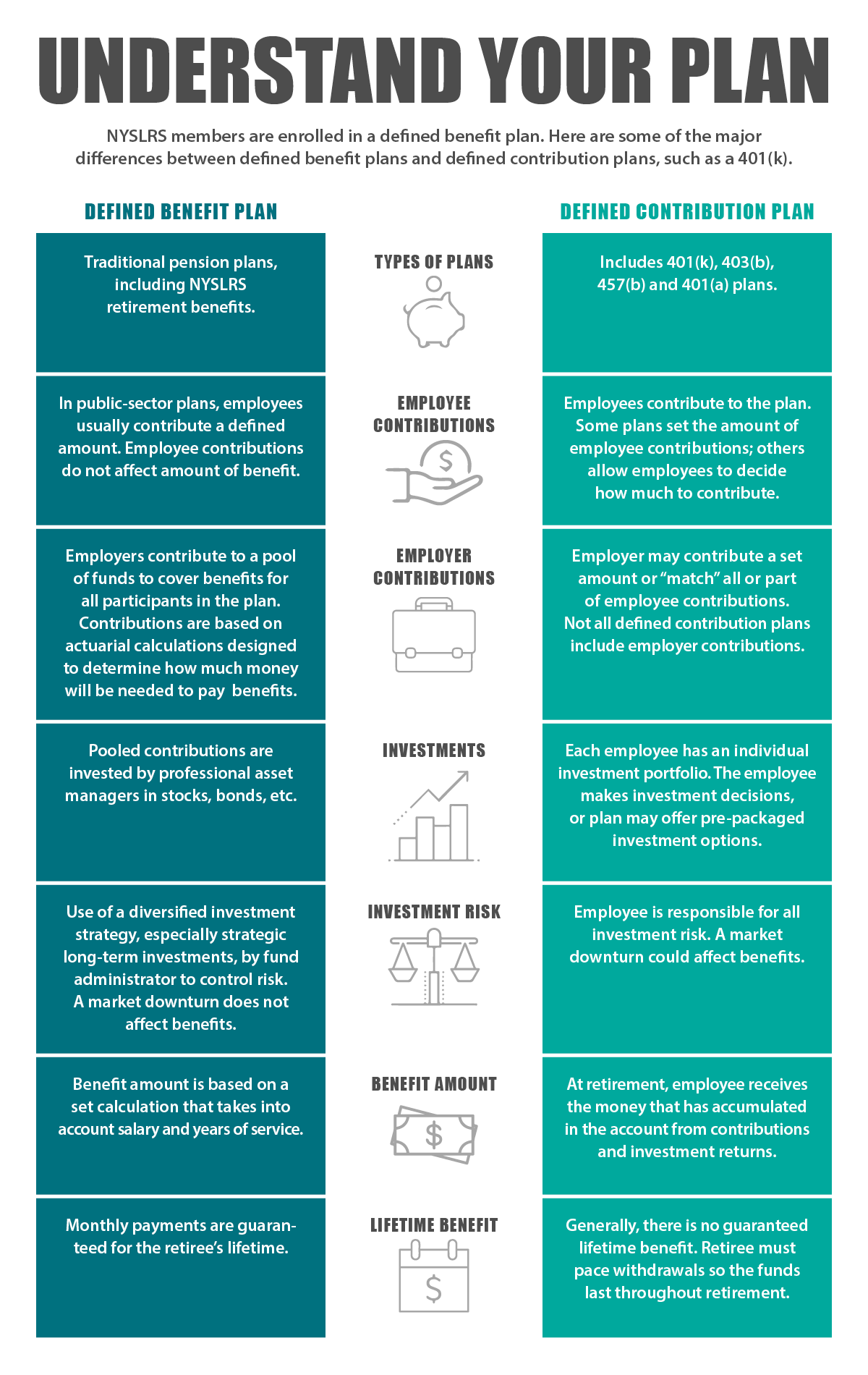

What is a Defined Benefit Plan? - New York Retirement News

What happens to my pensions after death? | The Private Office

हमारा_सैनिक_हमारा_स्वाभिमान... - I ...

DEATH BENEFIT NOMINATION FORM

Are Pension Death Benefits Taxable?

Chancellor abolishes 55% tax charge on death | Harding Financial

The death of retirement is looming – and the fallout will be ...

Untitled

The spousal bypass trust | Tax Adviser

Death benefits from defined contribution schemes

Pensions crisis - Wikipedia

What is a Defined Benefit Plan? - New York Retirement News

Pension death benefits 'indefensibly generous' | Financial Times

What happens to your pension when you die? - Aviva

Thierry verkest

Untitled

What happens to pension policies and life assurance policies ...

Fact Sheet Investor

PENSIONS - TAX TREATMENT ON DEATH

Death benefits from defined contribution schemes

Death & Survivor Benefits | The Western Conference of ...

INFORMATION NOTE ON THE NATO DEFINED CONTRIBUTION PENSION SCHEME

Now NPS will cover with Retirement Gratuity and Death Gratuity

Untitled

0 Response to "41 defined contribution pension death"

Post a Comment